The WISH Act probably isn’t going anywhere, but it’s interesting anyway . . .

Blog

Forbes post, “Do Teachers And Public Workers Without Social Security Lose Out? A New Analysis Says, ‘Sometimes’”

Originally published at Forbes.com on August 2, 2021.

Conventional wisdom says that the reason for public sector pension plans’ poor track record on funding levels is that benefit levels are simply too high, causing politicians to kick the can down the road perpetually. In Illinois, for example, “Tier 1” teachers can retire at any age, after 35 years of service, without any reduction to their benefit, and receive 75% of their pay with automatic 3% increases each year. As a bonus, they can add to their service calculation two years of unused sick leave, as well as non-vested time spent teaching out-of-state, if they pay the employee contribution (but not the employer cost) for that service. You simply can’t beat that in the private sector, even considering Social Security benefits.

But that’s not always true. Illinois is one of 15 states which do not cover some or all of their employees in Social Security. Although these plans ought to provide benefits that are the equivalent of the combination of Social Security and a private-sector retirement plan, federal law requires that, at a minimum, they must provide benefits at least as good as those provided by Social Security, and has established a “Safe Harbor” formula that determines whether plans comply with these rules: if a plan pays a benefit of at least 1.5% of pay, averaged over the last three years of service, and beginning no later than Social Security retirement age, then the plan is considered “qualified” and the state/town/school district can opt out of Social Security.

This is a very narrow test, though, and individual teachers in those plans can end up losing out. The test allows states to establish vesting periods, in some cases in excess of what federal law permits for private sector plans, such as 10 years in Connecticut, Georgia, Illinois, and Massachusetts. (Strictly speaking, Social Security has a sort of “vesting” in its coverage requirements, but those are met by work history over multiple employers.) The test doesn’t question whether the benefits provide by the plan exceed the contributions required from the employees. It doesn’t take into account teachers who withdraw their contributions and lose their benefits. And it doesn’t require a cost-of-living adjustment, without which fixed-income pensions will lose ground relative to Social Security even if benefits are equal at retirement.

At the same time, some workers in these plans will get a full Social Security benefit even if they leave their public sector job before earning a vested benefit, or if their benefit is so low they take their refund of contributions instead, simply because they will have met their 35 years of Social Security earnings history required for a full benefit, and because Windfall Elimination Provisions don’t apply for retirees who worked for public sector employers if they don’t actually have public sector pensions. That’s not to say there are positives to the failings in public sector plan design, but that Social Security itself mitigates those failings.

It is with this in mind that the Center for Retirement Research published a brief in April summarizing its authors’ research on the question of how workers in these plans fare, overall, taking into account all of those systems’ workers, not merely those with careers long enough to benefit from the systems’ generosity for full-career employees. They used a set of assumptions to calculate workers’ lifetime pension wealth, and a counterfactual Social Security wealth, to calculate, across all employees in a system and their likelihood to make it to retirement, and based on the benefits available for newly hired employees (taking into account, that is, reductions for new tiers), the “wealth ratio” for a given plan. And, in fact, nearly half of those plans, or 43%, did not have benefits that were as good as Social Security, on average for all workers, using this more sophisticated analysis.

To be clear, that’s the percentage of plans; the authors did not provide an analysis of what percentage of workers ended up with lower-than-Social Security lifetime benefits. They did, however, perform their analysis for certain sample workers, finding that in 74% of plans, a low earner would be better off with Social Security.

And the authors did not provide a listing of which of the plans in their study were relatively more or less generous, nor whether more generous plans were more or less funded than the parsimonious ones, nor — considering that they evaluated only new hires’ benefits — whether those which are low, are low because those are plans which had historically been low, or reflect new benefit cuts in response to low funding ratios.

But even with those limitations, this study is an important data point, especially for those of us, including, yes, myself, who believe that a key piece of Social Security, and public pension, reform is for all Americans to participate in our national old-age social insurance system.

And if you ask yourself, “how can benefit plans which are so expensive that politicians can’t fund them properly, have such poor results in this analysis?” that demonstrates, in part, the extent of the inequality between some workers and others, that you get with these sorts of plans.

December 2024 Author’s note: the terms of my affiliation with Forbes enable me to republish materials on other sites, so I am updating my personal website by duplicating a selected portion of my Forbes writing here.

Illinois is Broken, Secretary of State Race edition

Non-Illinoisans, what does your Secretary of State do?

In some instances, state Secretaries of State made national news in the last election, due to the choices they made in modifying state election law or its implementation, due to COVID, and their validation of election results, most notably Georgia Secretary of State Brad Raffensperger, who even now shows up in news reports.

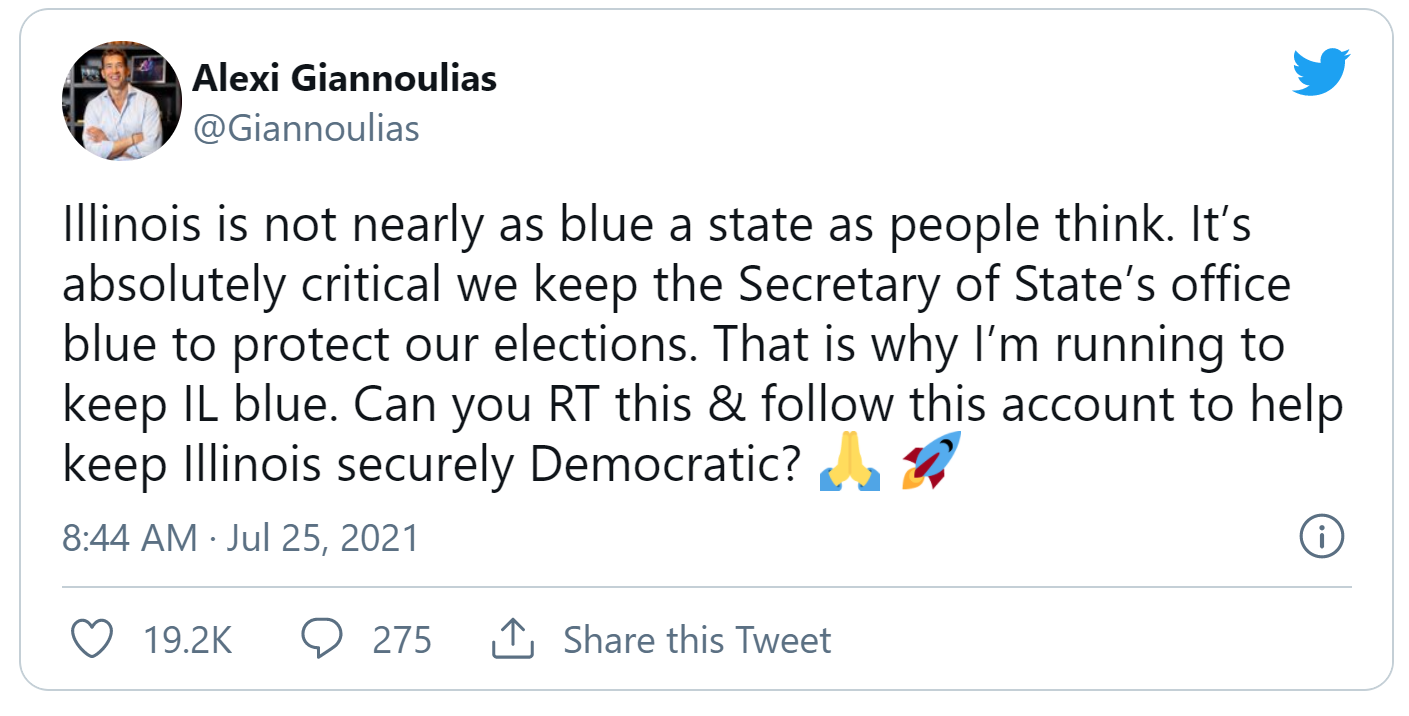

Which means that a non-Illinoisan might not think twice about this promise from Democratic candidate for the Illinois Secretary of State, Alexi Giannoulias (image posted at bottom in case of tweet deletion):

Illinois is not nearly as blue a state as people think. It’s absolutely critical we keep the Secretary of State’s office blue to protect our elections. That is why I’m running to keep IL blue. Can you RT this & follow this account to help keep Illinois securely Democratic? 🙏 🚀

— Alexi Giannoulias (@Giannoulias) July 25, 2021

And his website contains similar promises:

He supports Defending Voter Rights: “We must ensure access to registering to vote and individual rights at the ballot box are protected to prevent disenfranchisement.”

He advocates for Safeguarding Against Financial Fraud: “With the economic downturn making our most vulnerable citizens susceptible to fraud, deception and unfair practices, we must protect financial well-being of Illinois residents against those who prey on them.”

He promises he will go about Strengthening Ethics Laws: “With recent corruption scandals plaguing Illinois, we must toughen state ethics laws and reform the system to curb abuse.”

But in Illinois, the Secretary of State’s office is primarily Illinois’ equivalent to the Department of Motor Vehicles elsewhere, administering driving tests and issuing driving licenses and vehicle registrations, as well as secondary duties in administering the registration of corporations, lobbyists, and notaries, as well as overseeing the state archive and the state library. Were he to be elected, he would have nothing to do with voting (except for the minor element of “motor voter” registration), financial fraud (that’s the Attorney General), or ethics (that’s an office in the executive branch with no particular head other than the governor).

Giannoulias also promises he will “protect our privacy of Illinois residents and safeguard their data, photos and personal information from those who seek to abuse it,” and, sure, to the extent that the Secretary of State’s office holds data on Illinois drivers, there’s a privacy element, but this is small potatoes.

And he promises he will go about “making our roads safer” which sounds fine as far as it goes but then continues that he will do this by “strengthening safety guidelines for motorists and protecting the environment,” which seem to have a lot more to do with legislation than the administrative job of the Secretary of State.

Finally, he claims he will go about Modernizing Services: “COVID-19 has changed how all offices need to operate and deliver services – with the health and safety of the public a top priority – to improve the customer experience.” But this is trite and meaningless, all the more so since on his homepage he praises the outgoing Secretary of State, Jesse White’s “outstanding service.” And, to be honest, the Secretary of State took its time about implementing an appointment system for drivers’ license renewals, but now they have and it appears to work smoothly. And other than this, the biggest “customer experience” problem were the delays caused by the extreme length of time the office was closed, both in spring of 2020 and again over Christmastime — delays which may have been fine for many of those whose expiration dates were simply extended but caused significant difficulties for those seeking licenses for the first time. But his emphasis on “health and safety” suggests this is not a concern of his.

What it comes down to is this:

Alexi Giannoulias is not running for the office of Secretary of State.

What does he really want?

He is running to obtain the status of “next-in-line for governor.”

Here’s the Chicago Sun Times, from this past June:

Nevertheless, presiding over that state office is one of the most coveted prizes in Illinois politics.

“Next to being governor, that’s the biggest political office statewide,” said former Republican Gov. Jim Edgar. . . .

Political insiders say former state Treasurer Alexi Giannoulias is leading the pack, racking up crucial endorsements and building the most fully stocked political war chest. He is closely followed by Chicago City Clerk Anna Valencia, who has won her own share of endorsements, but in the money contest has so far been outraised by Giannoulias more than five-to-one. . . .

One of the allures of the office is its potential to serve as a political stepping stone.

Edgar, a former Illinois secretary of state who parlayed his tenure into a successful gubernatorial bid, said the current crop of candidates may be looking to do the same, since the office offers plenty of the tools to do so, from jobs to fill to publicity to take advantage of.

“You also have respect throughout the state. Your name — next to the governor’s — is the most visible name in state government, because you’re on everybody’s driver’s license,” Edgar said. “There’s a lot of political advantages.”

Now, to be sure, Giannoulias isn’t the only one doing this. Valencia’s website likewise claims new responsibilities for the Secretary of State, usurping the powers of the Illinois State Board of Elections, by calling for an “Illinois Voting Access Commission,” which would “bring together diverse stakeholders from across the State to identify ways to expand and protect voter registration, voting and vote counting. Our stakeholders will include the Illinois State Board of Elections, members of the Illinois General Assembly, County Clerks, community and business leaders, universities and foundations.” This commission would evaluate expanding Vote By Mail, Automatic Voter Registration, transportation to the polls, election judge recruitment, and would update voting technology — again, nothing that has anything to do with the roles of the Secretary of State. She would also create an “Illinois Civics Corps” — which would “give Illinois college students a stipend to register and educate their communities on how to become civically engaged.”

Again, none of this has anything to do with the responsibilities of the Illinois Secretary of State. (And, for that matter, none of the changes in election law in other states has anything to do with Illinois’ own election laws, and in fact, Illinois has been busy legislating expanded ease of voting, including expansion of vote by mail, expanded voting hours, and more.) Valencia is similarly trying to benefit from voters’ lack of knowledge, and their gullibility in believing that voting access is at risk and their association of state Secretaries of State with voting administration.

Now, in fairness, the three remaining candidates, Mike Hastings, David Moore, and Pat Dowell, make no such promises, touting instead their records of public service and business/oversight experience. But they are, as the Sun Times article states, the also-rans. And one of Giannoulias or Valencia will undoubtedly win, with Gianoulias’s ability to plaster the airwaves a definite advantage. Whether the winner then remembers that their job is limited to properly administering the Secretary of State’s office, or uses their platform to grandstand, or even abandons the public service daily grind in ways that cause hardship to Illinoisans just trying to go about their daily life, remains to be seen, but in any case this election will serve as a reminder that Illinois is fundamentally broken.

Forbes post, “What Millennials Really Think About Social Security – And Why They Might Not Be Entirely Wrong”

Originally published at Forbes.com on July 19, 2021.

What do Americans believe about Social Security? A new poll by Nationwide Financial, with splits by generation, gives us some answers. Here are four key items from the survey:

- Millennials are much less informed about the general nature of benefits: on average, this age group (ages 25 – 40) guessed that the full retirement eligibility age was 52 (compared to an average guess of 59 for Gen Xers (ages 41 – 56) and age 64, for Boomers and older; the actual age is, of course, age 67 for all but those closest to retirement.

- Generation Xers, on the other hand, have the least confidence in the security of Social Security funding — with 83% either “strongly” or “somewhat” agreeing that they “worry about the Social Security program running out of funding in my lifetime,” compared to 77% of Millennials and only 61% of Boomers and older.

- However, nearly half of Millennials, 47%, strongly or somewhat agreed that “I will not get a dime of the Social Security benefits I have earned,” compared to 33% of Gen Xers and 12% of Boomers and older.

- At the same time, over half of Millennials, 61%, agree or strongly agree that “Social Security on its own should be enough to help me live comfortably in retirement,” which is far, far more than the 41% of Gen Xers and 31% of Boomers and older.

What should we make of this?

The standard response to these survey results is to say something like this, quoting CNBC in an article titled (as is par for the course for this sort of article), “71% of Americans are worried Social Security will run out of money in their lifetimes. Why experts say that won’t happen”:

“The trust funds on which Social Security relies to pay benefits have been running low. The last official projection by the Social Security Administration indicated those funds could run out in 2035, at which point 79% of promised benefits would be payable. . . .

“Even so, fears that the program will run dry and benefit checks will stop are unfounded, said Shai Akabas, director of economic policy at the Bipartisan Policy Center. . . .

“’It is highly unlikely that it is going to disappear anytime soon.’”

But let’s give these respondents a fair hearing, rather than immediately writing them off as uninformed.

As to the apparent belief that Americans can collect Social Security far earlier than is actually the case, I can only guess that survey-takers misunderstood the question as I don’t believe it’s credible that substantial numbers believe they can actually collect Social Security so young. Perhaps they understood this to include eligibility for disability, perhaps they thought this was the age in which a person would have earned the minimum number of “coverage quarters” required, or something else. I tend to discard this answer as simply not meaningful.

Are Americans right to believe that Social Security may “run out of funding”? When it comes down to it, it’s a matter of interpretation: after all, I do believe it is very likely that Congress will not act before the Trust Fund runs dry, and that, regardless of when they act, it is highly likely that they will shift Social Security’s funding to that of ordinary tax revenues rather than a special Trust Fund. After all, the Trust Fund made sense when the program was established and it was intended that funds would build up for a time before being paid out, and again in the reforms of the 80s when Baby Boomers had hit their peak earning years, but now there is no such demographic bulge but merely an ever-diminishing number of workers relative to retirees. What’s more, the Democrat’s proposal for age 60 Medicare uses general revenues rather than a dedicated funding source. In addition, the child tax credits being celebrated now are being called “Social Security for children” despite any similar special “Trust Fund.” These developments, along with substantial plans for government spending expansion in general, make it all the more likely that the notion of a “Social Security Trust Fund” will not continue after its current funds are depleted.

Are Americans — and especially Millennials — right to suspect that they personally will not receive Social Security benefits? Again: it’s not unreasonable. In an environment in which there is so much talk of so much government spending, paired with seemingly endless partisan rancor, it indeed seems reasonable to surmise that the Social Security system, 27 to 42 years from now, could be much-altered and, quite possibly, be reserved for the poor. It seems rather likely that young adults in particular would believe that, regardless of their current finances, they would make their way up in the world to earning enough, relative to their peers, to be disqualified for welfare benefits.

Finally, again, in a world in which there is so much talk of a substantial expansion of government benefits, and so much disconnection of Social Security from its prior promise that is earned by paying into the system, it is no surprise that the majority of Millennials would view it as just another benefit system. Consider, after all, that 43% of Millennials support a “universal basic income,” compared to 37% of Gen Xers and 22% of Boomers, according to Victims of Communism polling; and that 47% of Millennials, compared to 39% of Gen Xers and 34% of Boomers, had a favorable opinion of the term “socialism.” If they believe that the government ought to, in a moral sense, be giving ordinary Americans more money than is now the case, it stands to reason that expectation would likewise be the case for Social Security. And, of course, the refrain of Democratic candidates during the last election was that they would “expand Social Security,” and surely far more voters heard that refrain, than dug into the details to learn the expansion promised was relatively small in scale.

What this boils down to, in the end, is not as simple as a throwaway explanation that Americans aren’t educated enough on Social Security. Rather, it seems more likely that their preferences have simply changed, compared to their elders — a change which may be positive, to the extent that it opens up opportunities for a complete redesign of the system, but may increase the difficulty of a successful political resolution, if too many Americans believe they can get the proverbial “free lunch.”

December 2024 Author’s note: the terms of my affiliation with Forbes enable me to republish materials on other sites, so I am updating my personal website by duplicating a selected portion of my Forbes writing here.

Forbes post, “The ‘Loneliness Epidemic’ Among The Elderly May Not Be What It Seems”

Originally published at Forbes.com on July 15, 2021.

“Loneliness and social isolation in older adults are serious public health risks affecting a significant number of people in the United States and putting them at risk for dementia and other serious medical conditions.”

That’s from the CDC, in their informational content titled, “Loneliness and Social Isolation Linked to Serious Health Conditions.” The material continues by saying that social isolation increases risk of premature death from all causes, at a risk level “that may rival those of smoking, obesity, and physical inactivity,” and that it increases dementia risk by 50%. In addition, loneliness was associated with higher rates of depression, anxiety, and suicide, and a nearly 4 times increased risk of death among heart failure patients.

But what are loneliness and social isolation? The CDC says,

“Loneliness is the feeling of being alone, regardless of the amount of social contact. Social isolation is a lack of social connections. Social isolation can lead to loneliness in some people, while others can feel lonely without being socially isolated.”

And here is the surprise: social isolation and loneliness are, for the most part, two entirely separate sets of circumstances. According to a new study, “The epidemiology of social isolation and loneliness among older adults during the last years of life” (paywalled, abstract here), significant numbers of the elderly, and, specifically, those within 4 years of death, were lonely and/or socially isolated. (This data comes from an ongoing study of the elderly, the Health and Retirement Study, or HRS, and uses only the subgroup of study participants who completed a survey, then died within 4 years.) Among this subgroup, 18.9% met the definition of being socially isolated — few or no household or local contacts such as children nearby; having infrequent contact with children, family, or friends by phone, e-mail, or in-person visits; and low levels of community engagement such as church attendance or community volunteering. In addition, 17.8% identified themselves as frequently feeling lonely. For survey participants who died no more than 3 months after completing the survey, a greater percent were socially isolated — 27% — but the increase in those reporting loneliness (from 19% to 23%) did not pass statistical significance tests.

Yet there is no correlation between these two characteristics — feeling lonely subjectively and objectively lacking in connections. (Strictly speaking, the correlation is 0.11, on a scale where 0 means no relationship at all and 1 means a perfect direct connection between the two.) Put another way, only 5% of people experienced both loneliness and social isolation, or, to do the math, 72% of those who reported being lonely were “objectively” not socially isolated — they went to church, volunteered in the community, talked to their children, but felt lonely anyway. And 74% of those who met the criteria to be labelled “socially isolated” did not feel lonely as a result.

What’s more, in 2018, Cigna commissioned a study on loneliness in adults, generally speaking. And here’s another surprise: they found that loneliness declines in older generations. Specifically, Generation Z (ages 18 – 22) had the highest “loneliness index”, at 48.3, and the index declined with each successive generation, with the Greatest Generation (ages 72+) coming in at a loneliness rating of 38.6. (Yes, as much as Gen X is usually dropped off of surveys as of no interest to researchers and the media, in this case the so-called “Silent Generation” is lumped in with their older siblings.) What’s more, those who are retired had the lowest loneliness index — 41.2 vs. 43.7 for the employed, 44.9 for homemakers, 47.9 for college students, and 49.1 for the unemployed.

Now, it’s not easy to compare apples to apples, but the two studies refer to the same basic assessment, the UCLA Loneliness scale, though the HRS asks only three questions and the Cigna study the full 20. Does the HRS version drop questions that would add greater precision to their definition of loneliness? Does the full 20 question version give excess weight to the way younger adults may experience loneliness? Maybe — the full and abbreviated questions are here; the three-question version asks about feelings of lacking companionship, feeling left out, and feeling isolated from others but omits questions such as “my social relationships are superficial” and “my interests and ideas are not shared by those around me.”

So what do we do with this? Solutions (such as those offered in an article at the Columbia Mallman School of Public Health) focus on what it calls “a new social infrastructure with attention to designing solutions to address the social needs of seniors and the needs for intergenerational connection,” suggesting co-housing communities, and mentioning in particular an intergenerational tutoring program to “address one dimension of loneliness: the need to be a contributor to the public good and have a role in a community with meaning and purpose.” As a personal anecdote, for years I had an elderly neighbor, childless and dependent on neighbors to check in on her, but who rejected activities at the senior center because “it’s full of old people,” and it does seem to be an operating assumption by many that the elderly will make great companions for each other simply because of their age, as if that’s their sole defining character trait.

In any case, this new data suggests that the “fixes” for loneliness and for social isolation — at any age — are simply not the same set of actions, whether by the government, non-profits, or communities.

December 2024 Author’s note: the terms of my affiliation with Forbes enable me to republish materials on other sites, so I am updating my personal website by duplicating a selected portion of my Forbes writing here.

Forbes post, “Do You Get Your Money’s Worth From Buying An Annuity?”

Originally published at Forbes.com on July 8, 2021.

Once upon a time, in the (somewhat mythical) past of traditional defined benefit pensions, your employer protected you from the risk of outliving your money in retirement, by acting, more or less, as an insurance company providing an annuity. With that benefit receding into the past, many experts have been hoping that Americans with 401(k) plans would avail themselves of annuities on their own, to give themselves the same sort of protection, and, indeed, the SECURE Act of 2019 made it easier for those plans to offer their participants an annuity choice, and, when surveyed, 73% of those participants said they would “consider” an annuity at retirement.

At the same time, though, Americans distrust annuities — in part because traditional deferred annuities had high fees and expenses and only made sense in an era predating IRAs and 401(k)s, when they were attractive solely due to the limited tax-advantaged options for retirement savings. But that’s not the only reason — annuities, quite frankly, aren’t cheap.

How do you quantify the value of an annuity? In one respect, it’s subjective and personal: do you judge yourself to be in good health, or does family history and your list of medications say that you’ll be one of those with the early deaths that longer-lived annuity-purchasers are counting on? Do you want to be sure you can maintain your standard of living throughout your retirement, or do you figure that you won’t really care one way or another if you have to cut down expenses once you’re among the “old-old”?

But measuring the value of annuities, generally speaking, does tell us whether consumers are getting a fair deal from their purchases, and here, a recent working paper by two economists, James Poterba and Adam Solomon, “Discount Rates, Mortality Projections, and Money’s Worth Calculations for US Individual Annuities,” lends some insight.

Here’s some good news: using the costs of actual annuities available for consumers to purchase in June 2020, and comparing them to bond rates which were similar to the investment portfolios those insurance companies hold, the authors calculated “money’s worth ratios” that show that, for annuities purchased immediately at retirement, the value of the annuities was between 92% – 94% (give-or-take, depending on type) of its cost. That means that the value of the insurance protection is a comparatively modest 6 – 8% of the total investment.

But there’s a catch — or, rather, two of them.

In the first place, the authors calculate their ratios based on a standard mortality table for annuity purchasers — which makes sense if the goal is to judge the “fairness” of an annuity for the healthy retirees most likely to purchase one. But this doesn’t tell us whether an annuity is a smart purchase for someone who thinks of themselves as being in comparatively poorer health, or with a spottier family health history, and folks in these categories would benefit considerably from analysis that’s targeted at them, that evaluates, realistically, whether annuities are the right call and whether their prediction of their life expectancy is likely to be right or wrong.

In the second place, the 92% – 94% money’s worth calculation is based on the typical investment portfolio of insurance companies, approximated by the returns of BBB-rated bonds. This measures whether the annuity is “fair” or not, in that “moral” sense of whether the perception that the company is “cheating” is customers is real (it’s not).

But these interest rates are very low. The authors, in addition to their calculations of “money’s worth,” back into the implied discount rate from the annuity costs themselves. For men aged 65, that interest rate is 2.16%; for women aged 65, 2.18%.

Now, imagine that you compare this annuity to an alternative plan of investing your money in the stock market, earning 7% annual returns, and believing you can predict your death date (or not really caring if you fall short or end up with leftover money for heirs). The cost of the protection offered by the annuity, the guarantee that you will never run out of money, and that you will not suffer from a market crash, is very expensive indeed — when you compare apples to oranges in this manner, the money’s worth ratio is, according to my very rough estimates, more like 60%, meaning that about 40% of your cash is spent to purchase the “insurance protection” of the annuity.

And, again, that’s not because insurance companies are cheating anyone; that’s solely because of the wide gap between corporate bond rates and expected returns when investing in the stock market— a gap which was particularly wide in the summer of 2020 when this study was competed, but remains nearly as wide now. As it stands, Moody’s Baa rates are in the 3% range; in the 2000s, they were in the 6% range, and in the 1990s, from 7% – 9%. Although this drop in bond rates is good news for American homebuyers because this marches in tandem with mortgage rates, it makes it far harder for retirees to manage their finances in ways that protect them from the risks that they face in their retirement.

Perhaps interest rates in general, and bond rates specifically, will increase as we leave our current economic challenges, but there’s no certainty, and as long as this gap between bond rates and expected stock market returns remains so substantial, retirees will be challenged to find any sort of safe investment that makes sense for them. Which means that what seems like a great benefit for Americans looking to borrow money — for mortgages, car loans, credit cards — can pit the elderly against the young in a generational “us vs. them” contest.

December 2024 Author’s note: the terms of my affiliation with Forbes enable me to republish materials on other sites, so I am updating my personal website by duplicating a selected portion of my Forbes writing here.

Forbes post, “Will New Jersey Fund Pensions With Stealth-Taxes? An Asset Transfer Update”

Originally published at Forbes.com on July 2, 2021.

New Jersey, the only state to have a pension funded status worse than Illinois’s (according to Pew’s 2020 compilation based on 2018 data), is quite pleased with itself because, as the state announced in a recent press release,

“State Treasurer Elizabeth Maher Muoio announced that the Treasury Department today kicked off the start of the new fiscal year by paying the full state-funded portion of the $6.9 billion pension contribution slated for Fiscal Year 2022 (FY 2022). This marks the first time in more than 25 years that New Jersey is making the full Actuarially Determined Contribution to the Pension Fund, plus an additional $505 million contribution, and also the first time in years that the state has made a lump sum payment, rather than quarterly payments.”

And Senate President Stephen Sweeney believes he has a solution to reduce the burden of these pension payments, in the form of the Retirement Infrastructure Collateralized Holdings Fund (yes, the “RICH Fund”), as proposed in legislation being considered by the New Jersey Senate, which he promotes in a commentary at NJ Spotlight News. He writes,

“That is why we have developed legislation to enable our state and local pension systems to add revenue-generating assets like water and sewage treatment systems, High Occupancy Toll (HOT) lanes, parking facilities and real estate to provide new, diversified sources of revenue for their investment portfolios.

“Senate Bill 3637, which may be considered by the Senate Budget and Appropriations Committee this week, would create the Retirement Infrastructure Collateralized Holdings Fund — RICH, for short — as an infrastructure trust fund to hold and manage assets transferred to the public corporation by state and local governments for the benefit of New Jersey’s public employee pension funds.

“This would not only bolster the pension system, but also give state and local governments powerful new tools for preserving public ownership, improving public stewardship, and maximizing public benefit. . . .

“The state and local governments own water systems, reservoirs, real estate and parking lots that could generate stable revenue for pension systems in the same way that the Lottery system has for the past several years.”

But none of the assets listed, when publicly-owned, are intended to be profit-generating! People expect their water treatment and sewage-treatment systems to operate at cost, to provide clean water and dispose of human waste in a sanitary manner, to protect public health. We expect our government officials to manage these systems at a cost that’s as affordable as possible while still keeping systems in good repair, and all the more so for the sake of the low-income among us. To be sure, private companies are gaining market share in the United States, providing water for one in six Americans, according to The American Prospect. And while the rationale for privatization can potentially be sound — the inability of a municipality, especially a small one, to fund needed improvements, and the expectation that a large multinational can manage more effectively, generally-speaking — too often (as reported at the Philidelphia Inquirer) towns simply perceive of it as a quick cash infusion, regardless of the long-term cost to residents in the form of higher rates. (And, yes, Chicagoans will be quick to share their painful experience with parking meters, 75 years’ of revenue from which was sold to a private company for a one-time cash payment of $1.16 billion, in a 2009 transaction under former mayor Daley.)

In other words, when these components of core public infrastructure become a source of profit, it is a sign not of sound governance, but of misgovernment. Any instance in which the management of a system of infrastructure is contracted out to a private entity, should be limited to cases in which that private entity can better manage the system, and earn a profit from the savings derived from superior management. Handing over such an asset to a public fund, which would in turn need to contract with a third party to manage the asset, would not suit the bill.

What it comes down to, then, is that Sweeney is proposing to fund state pensions through a set of taxes which are hidden to the public. How many residents, after all, when they see their water bill go up, or pay more on the toll roads, will be aware that these new rates are for the purpose of funding pensions? What’s more, these sorts of revenue-raisers are far more regressive, with higher relative costs for lower-income residents, than a simple income tax. No one should be patting themselves on the back as if they have come up with an innovative solution here!

Perhaps it’s for this reason that Illinois abandoned its plan to fund pensions through asset transfers — not with a public announcement, of course, but simply by letting the task force die a quiet death, never releasing the draft report its members had prepared. At least in this respect, Illinois appears to have dodged a bullet.

Update: the bill died so is seemingly not worth duplicating at this website; however, the “solution” appears to pop up every now and again and the general principles of why to reject it are unchanging.

December 2024 Author’s note: the terms of my affiliation with Forbes enable me to republish materials on other sites, so I am updating my personal website by duplicating a selected portion of my Forbes writing here.

Forbes post, “Taking Labor Shortages Seriously – Economywide”

Originally published at Forbes.com on June 21, 2021.

“Emilio Enriquez has climbed from busser to line cook during his seven years working in restaurants, and he still dreams of becoming a chef.

“But he hasn’t worked during the COVID-19 pandemic and won’t look for a job until fall, once unemployment benefits no longer pay more than he would likely earn working and, he hopes, more people are vaccinated.

‘This is what I want to do in the long haul,’ said Enriquez, 25. ‘I’m just not ready to do that yet — especially since I’m making more at home.’”

These paragraphs — the opening paragraphs of a front page article in the Chicago Tribune earlier this month — are a rare instance of a journalist openly citing a nominally-”unemployed” individual choosing to stay out of the job hunt until after unemployment runs dry; far more often newspapers claim that these individuals just don’t exist, that the folks continuing to collect unemployment are truly unable to find work or truly prevented from working due to child care difficulties.

The remainder of the article discusses the labor shortage in the restaurant industry, from servers and bartenders to dishwashers and cooks. Industry experts reported that former employees had found work in other fields: “cannabis, distribution centers like Amazon and UPS, delivery services,” and the article interviewed half a dozen people, most of whom indicated plans to return to college in the fall instead of returning to a restaurant-industry job. Among the complaints cited by these workers, as well as by an advocacy group, One Fair Wage, were low pay, unpredictable and late hours, harassment from customers or co-workers, failure to follow safety requirements, and the health effects of exposure to sanitization chemicals.

What’s the fix? The industry representatives cited did not promote ending the bonus unemployment benefits. Instead,

“The biggest fix, [Hopleaf owner Michael] Roper said, would be “a rational immigration policy” that welcomes the people who do much of the hard labor in the United States. [Illinois Restaurant Association president Sam] Toia also championed immigration reform to boost the service industry, including an immigrant work visa program endorsed by the National Restaurant Association.”

But let’s set aside the issue of the $300 weekly unemployment bonus. Let’s take people at their word that this is a longer-term issue that has to do with the unattractiveness of restaurant work rather than government benefits, paid out on the premise that no work is available, leading people to turn down work. What’s to be done? It would seem obvious that the answer is simply for those complaining restaurants to boost their wages to a level that makes those jobs attractive despite the late hours. The reality is, of course, that to do so would require boosting menu prices, a change which results not only in fears of inflation, but (and this is less discussed) will sooner or later result in customers dining out less often or choosing less expensive restaurants. But that’s not necessarily objectively a bad thing; there is, after all, no need for any given frequency of restaurant dining for one’s well-being, and a change in pay scales would simply change norms and expectations about frequency.

Yet, at the same time, the industry’s proposed solution, increases in immigration, hardly seems like the ethical and responsible solution if, indeed, the worker shortage is due to poor pay and job conditions in an objective sense, rather than due to a spectacularly-booming economy in which workers have their pick of any number of jobs with “living wage” salaries and benefits. Why would it be appropriate for a restaurant to obtain a work visa with which to pay an immigrant low wages, if those wages would create a class of workers with living standards which we deem too low for Americans? Is it ever acceptable to create a set of jobs with low pay rates (that is, by using immigration increases to prevent wage increases which labor shortages would otherwise generate), with the rationalization that the families those workers are supporting live overseas in countries with lower costs of living?

Right now we’re discussing this with respect to restaurants, because that’s highly visible to those of us economically prosperous enough to visit restaurants and see the labor shortage play out: the host who says, despite clearly empty tables, that it’s a wait to be seated. But readers can likely guess where I’m going with this: there has been a longstanding labor shortage with respect to home care workers and caregivers at nursing homes and related facilities. Is the solution to boost wages? To hire workers from overseas? To do both — boost wages and hire immigrant workers?

Wage hikes, of course, increases costs both for the government and for families who pay their expenses on their own. Where there are fixed governmental budgets, that means more families on waiting lists. For families, that means more making-do, family members providing care, or going without or with less care, and, ultimately, means finally answering the question of whether the federal government should pay eldercare expenses for middle-class elders as well as for the poor, and whether children of those elders have obligations to support their parents (in Germany, for instance, those earning over EUR 100,000 have a legal obligation to pay their parents’ eldercare costs).

The latter — well, it’s a whole ‘nother kettle of fish. In 2019, the organization LeadingAge launched an initiative it called the IMAGINE Initiative, which proposed a set of immigration changes to boost the number of immigrants working in elder care. The proposal cites models overseas, such as 5 year temporary employment for foreign eldercare workers in Israel and a program giving eldercare workers permanent residency in Canada if they complete two years of live-in caregiving. For the United States, they suggest a six-year guest worker program specifically for elder caregivers, carve-outs in the EB-3 professional immigrant program for CNA and RN positions, creating a loophole in the R-1 program for religious workers to include non-US elder caregivers employed by religious organizations, the creation of an au-pair-equivalent program requiring eldercare rather than child care, allowing more temporary immigration in the NAFTA-replacement free trade agreement with Mexico, and directing an increased number of refugees towards eldercare employment.

These proposals bear no little resemblance to guest worker programs in oil-rich countries, in which foreign, temporary workers account for the largest part of the workforce and in which, except for professional workers, those workers much leave spouses and children behind in their home countries. We tend to think that in these countries, the prevalence of foreign workers is a marker of the spectacular wealth of those countries, but that’s not necessarily the case: in Saudia Arabia (or at least as of a decade ago), 90% of all private-sector workers were foreign workers, while at the same time 40% of all Saudi citizens lived in poverty.

Adding to these issues the overall uncertainty about the impact of future fertility rates and automation on the economy, and there simply is no easy solution here.

December 2024 Author’s note: the terms of my affiliation with Forbes enable me to republish materials on other sites, so I am updating my personal website by duplicating a selected portion of my Forbes writing here.